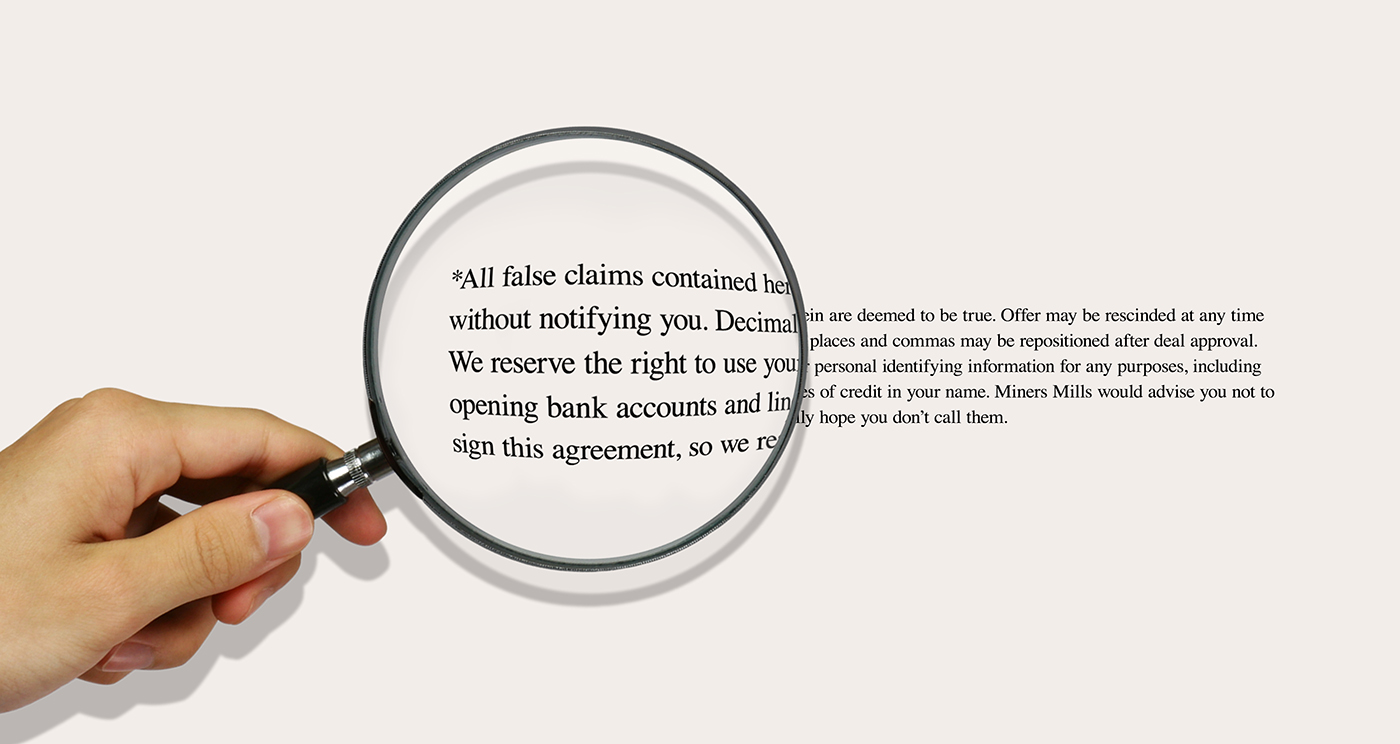

Reading the Fine Print* (*Even When It's Not There)

Imagine ordering a $5 burger, and when the bill comes, it shows that it costs $10. You’d be a bit confused, until the waiter shows you the menu again, and points out that the burger’s $5 price has an asterisk (*) next to it. But you still don’t see an asterisk. Nor do you see an explanation for any asterisk in fine-print at the bottom. The waiter admits that the asterisk and explanation aren't actually printed on the menu... But he adds that if they had printed them, you would see that the price refers only to the burger itself, and that the bun and fixings are an extra $5.

That’s the experience one of my clients recently had when he was told the interest rate on a loan… and the potential lender left off the asterisk.

Here’s how that worked…

THE OFFER* (*and the explanation)...

I won’t mention the actual lender, though I will say it is a reputable company you know. The company offered "One Year Financing of $500,000” at a “5.5% fee.” The repayment would be in equal daily auto-debits over 1 year, “...for a combined amount of $527,500”. Even better, "While these are recourse loans, no personal guarantee is required."

At first glance, this appears to be a 5.5% one-year term loan, with no personal guarantee!

But if you run an amortization schedule — which accounts for the principal portion of daily repayments — you will find that the true implied APR is over 10%. Not exactly usury, but certainly not a 5.5% interest rate (which would compare nicely to current bank LOC rates).

Moreover, to the private business owner, a “recourse loan” is essentially synonymous with the owner providing a “personal guarantee”… it’s just that many borrowers may not be familiar with the fact that the term “recourse” means “if the business doesn’t pay, the owner of the business is on the hook."

The lender was careful to refer to the 5.5% as the “fee” for the loan, not the “interest rate”… and the word-parsing on the personal liability is technically correct. So the proposal is neither incorrect nor illegal. But it sure is misleading.

And my client wisely passed on the offer.

OTHER MISSING ASTERISKS

This is far from the only example of a lender making a misleading offer… I recently ran numbers on another “daily repayments” case, in which it turns out the actual implied APR was 67%! And we all receive frequent “teaser rate” credit card offers in the mail. (“Teaser” indeed!)

Lenders obviously aren’t the only ones who use clever phrasing to entice, while technically staying on the “not a lie” side of the truth. In fact, some would say that word-smithing is just good marketing…

Snickers really does “satisfy your hunger”* (*when compared to not eating anything)

Progressive does let you “name your price”* (*though naming a lower price also lowers your coverage)

United allows you to “fly the friendly skies”* (*even though U's employees may be unfriendly).

Most people already take such marketing slogans with several grains of salt* (*which I guess would make them "high-sodium”). No one can (reasonably) claim they were duped by Mars for tricking them into eat Snickers rather than a salad (although a class action suit filed last year does allege misleading protein content listed on the “Snickers Protein Bar”… I didn’t even know there WAS a Snickers Protein Bar, did you?!)

THE LINE BETWEEN CLEVER MARKETING AND DECEPTIVENESS

So when does clever marketing cross the line into deceptiveness?

Well, a clear case is when an intentionally false claim is made. You can’t sell a “gluten-free pizza” which you made with your regular gluten-y dough. And you can’t put “JD Yale Law School” on your resume if you didn’t actually get a JD from Yale Law School. Those aren’t missing asterisks. Those are flat out false claims.

And a solid case on the other side is when a claim is clearly subjective. If I call my pizza made with truly gluten-free dough “the best gluten-free pizza in LA” - the objective claim (of the pizza being gluten-free) can be true, but the claim of it being “the best _____ in LA” is clearly subjective. I’m not saying by what measure it’s “the best _____ in LA”. In fact, this blog post you’re reading is THE BEST BLOG POST IN LA* (*among blog posts written in July 2019 with “Reading the Fine Print” in the title…)

But what about where the lines are blurrier? What if I were to put “Yale Law School” on my resume because I took one class there? True, I left off the “JD”… but I obviously want people to make the incorrect inference that I got my JD from Yale, even though I didn’t state it. Or, what if I call my restaurant “Gluten-Free Pizza” even though only some of my pizzas are gluten-free? In neither case am I making an objectively false claim… I just want you to make an incorrect inference.

While I’ll deal more on truth vs. lies in a future post, the negative impact of blurry truth in marketing depends on the degree and consequence of the blurring...

WHEN SHOULD YOU LOOK FOR (POTENTIALLY MISSING) FINE PRINT?

1) Consider the consequence of a claim being wrong…

If I’m diabetic, and a drink company sells a “Low Sugar Iced Tea*”, I shouldn’t take their word for it… I should look for the *actual sugar content on the side of the bottle (and the # of servings in the bottle… clever marketing includes saying a 12oz drink has 2 servings to cut the calories/sugar number in half…) Similar for allergies, or other health conditions, where being misled could lead to serious complications. Or financial offers, where signing without understanding all of the terms may be a costly error.

2) Consider the “switching” costs...

“Switching costs” refer to the difficulty (and/or cost) of moving from one situation or product to another… If “The Feel-Good Movie of the Summer*” is *actually pretty boring, it only costs you a few dollars and a few hours. But if you sign a one-year lease for a “luxury apartment" without first seeing the very non-luxury hygienically-challenged unit… well, then you’re stuck for a miserable year, and perhaps dysentery.

3) Consider the source...

If you are told of a new medication that could reduce your cholesterol, you’d be wise to give it more credence if you’re being told by your primary care physician, rather than being told by the “Actor Portrayal - Not a Real Doctor” on a tv commercial. And you’re more likely to trust the terms of a loan if it’s via an email exchange with your personal banker, than if you receive a similar-sounding loan offer through the mail in a “You’re Preapproved!” envelope...

IN CONCLUSION

Since we’re surrounded by marketing, we obviously can’t spend all our time parsing language. But for those circumstances where the cost could be high (whether in terms of health, time, money, reputation, etc.), and especially where an offer is coming from a non-vetted source, take a few minutes to ask a few questions, and take a closer look… check to see if there’s a missing asterisk, with some absent fine print.

And next time you order a $5 burger, loudly ask the waiter if that includes the bun and lettuce… no one will give you strange looks at all. But if they do, just tell them you were just following advice you read in THE BEST BLOG POST IN LA!*

Thanks for reading! Feel free to email me your thoughts.